The Taxation of Couples

Abstract

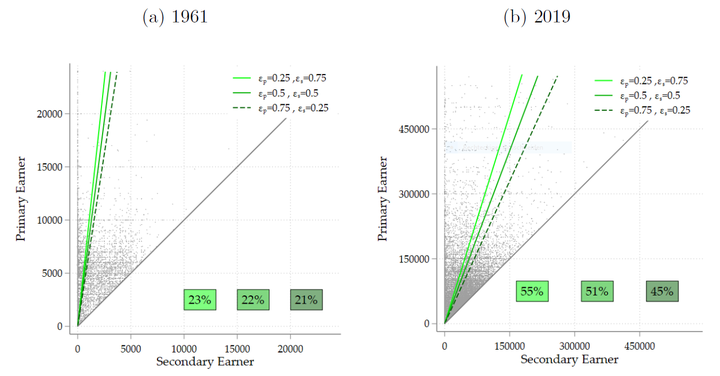

This paper studies the tax treatment of couples. We develop two different approaches. One is tailored to the analysis of tax systems that stick to the principle that the tax base for couples is the sum of their incomes. The other is tailored to the analysis of reforms towards individual taxation. We study the US federal income tax since the 1960s through the lens of this framework. We find that, in the recent past, realizing efficiency gains would have required lowering marginal tax rates for secondary earners. We also find that revenue-neutral reforms towards individual taxation are in the interest of couples with high secondary earnings while couples with low secondary earnings are made worse off. The support for such a reform recently passed the majority threshold. It is rejected, however, by a Rawlsian social welfare function. Thus, there is a tension between Rawlsian and Feminist notions of social welfare.